The Register of Overseas Entities: What is it and what do overseas entities need to do?

The Economic Crime (Transparency and Enforcement) Act 2022 (ECA) is a historic piece of legislation which introduces significant reform to the registration regimes at Companies House and Land Registry by creating a new Register of Overseas Entities (ROE). The ROE went live on 1 August 2022 and raises a series of important obligations for overseas entities.

The ECA creates a new ROE at Companies House which contains details about overseas entities which own UK property. For the purposes of the ECA, an overseas entity is a company or other entity such as a partnership or trust that has a legal personality under its governing law and is governed by non-UK law.

The rationale behind the creation of the ROE

Overseas entities can sometimes be used to conceal and launder the proceeds of crime. This is primarily due to a lack of transparency around the ultimate ownership and control of such entities. The ECA and ROE seeks to address this issue – and therefore facilitate the identification of the owners behind such overseas entities and prevent land being used for money laundering purposes in the UK – by creating an up to date public register which contains verified details of the ultimate beneficial owners of overseas entities who own UK property.

The legislation was expedited through Parliament as a result of the Russian invasion of Ukraine.

Overview of legal position

Requirement to register on the Register of Overseas Entities

An overseas entity must, unless it is an exempt overseas entity (see note below), apply at Companies House for registration on the ROE if it:

- (i) currently owns a Qualifying Estate (see below) and became the registered owner at the Land Registry of that Qualifying Estate pursuant to an application for registration made on or after 1 January 1999; or

- (ii) is purchasing / has purchased a Qualifying Estate and is applying to the Land Registry to become the registered owner of a Qualifying Estate on or after 5 September 2022.

Qualifying Estate means a freehold property or a leasehold interest granted for a term of seven years or more in the UK.

Note: There is currently no guidance on what constitutes an exempt overseas entity. The secondary legislation dealing with this has not yet been published.

How to become registered

To register on the ROE, an overseas entity must deliver to Companies House an application for registration along with the following:

- (i) a statutory statement relating to the identity of its registrable beneficial owners (see below);

- (ii) a statement confirming that the overseas entity has taken reasonable steps to identify all of its registrable beneficial owners and obtain the information required;

- (iii) verification in respect of the identity of its registrable beneficial owners or managing officers (as applicable); and

- (iv) the name and contact details of an individual who may be contacted about the application.

The verification checks on the registrable beneficial owners referred to at (iii) above must be carried out by a UK registered agent (Verification Agent) no earlier than three months before the application is submitted and will include ID checks.

To avoid issues arising around the registration process and to prevent any inconsistencies between the information supplied to Companies House and the information given to the Verification Agent, it is recommended that the Verification Agent carries out the verification checks and also submits the application for registration (rather than the overseas entity (or other person) trying to submit the information to Companies House themselves).

Blake Morgan LLP does not carry out this service, but a list of Verification Agents can be found here.

Note that Verification Agents will charge a fee for this service and Companies House also charge £100 for each application.

Once registered, the overseas entity will be allocated an overseas entity ID, and must ensure that the ROE is updated on at least an annual basis by delivering a statement confirming whether its registrable beneficial owners have changed since the last update.

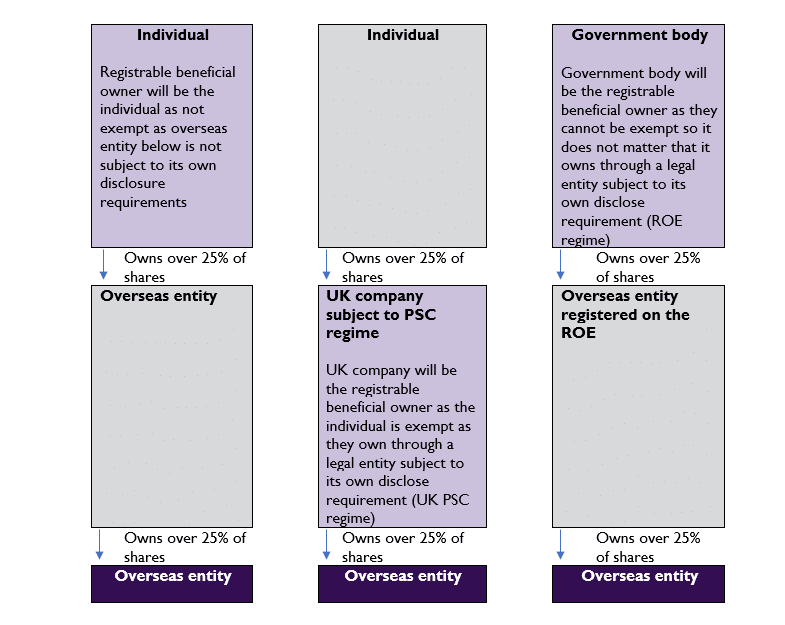

Who are the registrable beneficial owners?

Before applying to be registered on the ROE, the overseas entity will need to identify any registrable beneficial owners it has and obtain information about them. This regime is modelled on and aligns closely with the PSC (person of significant control) regime for UK companies.

There are detailed criteria surrounding who constitutes a registrable beneficial owner, and Verification Agents can help in this regard. However, generally, a registrable beneficial owner will be someone who:

- (i) directly or indirectly holds more than 25% of the shares or voting rights in the overseas entity; or

- (ii) has the right directly or indirectly to appoint or remove the majority of the board of directors of the overseas entity; or

- (iii) otherwise exercises or has the right to exercise significant control or influence over the overseas entity; and

- (iv) is an individual or a legal entity with its own disclosure requirements (see below), unless they are exempt or a public or governmental authority.

Legal entity subject to its own disclosure requirements – this includes, for example:

- a company which is subject to the UK PSC regime;

- a company with voting shares traded on a UK or EU market; and

- another overseas entity registered on the ROE.

Exempt – an individual or legal entity will be exempt from being a registrable beneficial owner if:

- (i) they only hold their interest in the overseas entity through one or more other legal entities, and are a direct or indirect beneficial owner of each such legal entity; and

- (ii) one of those legal entities is a beneficial owner of the overseas entity and is subject to its own disclosure requirements.

Note that a government or public body cannot be exempt.

Examples

An overseas entity will need to serve a notice on any persons or entities that it believes is a registrable beneficial owner or may know who the registrable beneficial owners are. This notice must ask for the information required for the Companies House application.

The person receiving such a notice must reply within one month and will commit an offence if they don’t reply or if they knowingly or recklessly provide false information.

If an overseas entity believes that it has no registrable beneficial owners, it must provide verified information about its managing officers.

Land Registry

From 5 September 2022 onwards, the Land Registry has been entering restrictions on the Land Registry titles of Qualifying Estates owned by overseas entities pursuant to applications for registration made on or after 1 January 1999. Such restrictions will prevent the registration of a disposition of a Qualifying Estate (subject to certain exceptions as referred to in ‘Enforcing security’) unless and until the overseas entity has registered on the ROE (unless it is exempt) and is up to date with its registration updates. The dispositions caught by the restriction include a transfer, the grant or assignment of a lease for a term of seven years or more, and the grant of a legal charge.

An application by an overseas entity to register its acquisition of a Qualifying Estate which is submitted from 5 September 2022 onwards will not be accepted unless the overseas entity is on the ROE (or is exempt), and a restriction (as referred to above) will be entered on the Land Registry title of the Qualifying Estate on completion of the application.

Key dates

For an overseas entity which became the registered owner of a Qualifying Estate pursuant to an application for registration made on or after 1 January 1999 but before 5 September 2022, the deadline for submitting an application to register on the ROE was 31 January 2023 and the Land Registry restriction on the Qualifying Estate’s title became effective on 1 February 2023.

If an overseas entity made a disposition of a Qualifying Estate between 28 February 2022 and 31 January 2023 (inclusive), it will need to have either:

- (i) registered on the ROE or submitted a pending application to be registered (providing details of the disposal as part of its application); or

- (ii) provided to Companies House the details set out above in ‘How to become registered’ along with details of the relevant disposition, even if it no longer owns any Qualifying Estate,

in each case by 31 January 2023.

If the overseas entity submitted an application to be the registered owner of the Qualifying Estate on or after 5 September 2022, the entity will need to be registered on the ROE before submitting their Land Registry application.

Companies House and the Land Registry have sent letters to overseas entities that it believes should be registered on the ROE.

Consequences of non-compliance

1. Failure to register

If an overseas entity (which is not exempt) is not registered on the ROE or does not have a pending application to register on the ROE in accordance with the key dates above:

- (i) where the overseas entity is acquiring the Qualifying Estate, it will be unable to register itself as the legal owner of the Qualifying Estate at the Land Registry and so will only have equitable ownership; or

- (ii) where the overseas entity is already the registered owner of the Qualifying Estate (subject to the key dates above):

- (a) the overseas entity and its officers in default will have committed a criminal offence punishable by fines (of up to £2,500 per day), imprisonment (of up to two years) or both;

- (b) the restriction will prohibit the registration of a disposition (subject to the specified exceptions as referred to in ‘Enforcing security’) of the Qualifying Estate; and

- (c) if the overseas entity enters into a transaction in breach of the restriction, it and its directors will have committed a criminal offence punishable by fine, imprisonment (of up to five years) or both.

A failure to be registered on the ROE will not invalidate the transaction which the overseas entity has entered into (subject to the terms of that transaction). However, it will impact its registration at the Land Registry and this in turn will impact the legal and equitable rights of the relevant parties created by the transaction, as well as the overseas entity and its officers who will be in default and will have committed an offence punishable by fine.

If an overseas entity has missed the deadline of 31 January 2023 for registration on the ROE, it should submit an application for registration as soon as possible to avoid and/or mitigate against any penalties described above.

2. Failure to update ROE

If a registered overseas entity fails to keep the ROE updated, its registration on the ROE will be deemed void and ineffective until it has delivered to Companies House the required updated information. This means that any disposition of the Qualifying Estate will be caught by the restriction on the Land Registry title and the overseas entity and its officers who are in default will have committed an offence punishable by daily fine as described above.

For Government guidance on the ROE regime see here.

Share:

![]()

![]()

![]()

If you need banking or financial legal advice

Speak to one of our specialist lawyers

Arrange a callHOW CAN WE HELP?

To get in touch with one of our legal experts please fill in your details.

Enjoy That? You Might Like These:

events

articles

articles